What to Do With Your Savings in UAE: Escape the Save-Spend-Save Loop

Money Saved Is Money Waiting to Be Spent elsewhere…

And money invested?

It has great potential to grow into lasting wealth!

If you have built up savings in UAE and are wondering how to put it at work, this post is for you. Because in my 14+ years advising expats in Dubai, I’ve seen the same two patterns play out again and again — and both quietly destroy wealth.

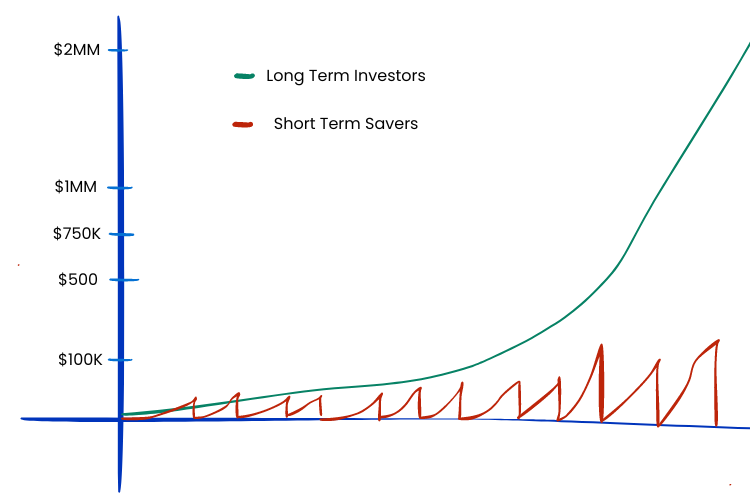

The Save–Spend–Save Loop

Most expats in the UAE are good at saving.

But here’s the part no one talks about: those savings often don’t last long.

They save diligently. But when their savings hit a mental threshold — usually 3 to 6 months of income — they feel compelled to do something with it.

And more often than not, that “something” is spending.

- A holiday comes up.

- A car upgrade feels justifiable.

- A family obligation demands attention.

And just like that, the money sitting in their bank account is gone — spent elsewhere. They’re pushed back to square one.

Sound familiar?

The Psychology of Short-Term Saving

I’ve met many expats who’ve lived in the UAE for years — yet they don’t have even 2–3 months’ worth of emergency savings.

They’re constantly caught in the loop… unable to break free.

They save with intention. They feel secure. But without a bigger plan, saving becomes temporary — just a pit stop between paychecks and purchases.

I call it Short-Term Saving Syndrome.

It’s not that they’re bad with money. It’s just that their money doesn’t have a purpose beyond the next spend.

If you’re still working on building that first buffer, start with my guide on how to save money in Dubai — then come back here for what to do once you have.

When Money Sitting in Your Bank Account Becomes a Trap

On the other end of the spectrum, I also meet expats who are incredibly disciplined savers.

Some have AED 500,000… a million… even more — just sitting in their bank accounts, untouched.

In fact, I’ve seen people with 10, 20, even 30 times their monthly salary parked idle in the bank. They feel secure. In control. Cautious.

But here’s the uncomfortable truth:

That money isn’t working for them — it’s just waiting to be spent.

They don’t lose it. But they don’t grow it either. With inflation quietly eroding purchasing power every year, money sitting in a bank account is actually losing value in real terms.

Wealth doesn’t grow in still water — it flows with direction.

That’s why knowing what to do with your savings — not just accumulating them — is the key to building long-term financial freedom in the UAE.

What to Do With Your Savings in the UAE: A 4-Step Plan

So whether you’re stuck in the save-spend loop or sitting on a large idle balance, here’s a smarter path forward.

Step 1: Separate Your Emergency Fund From Your Investable Savings

Before deciding where to invest savings in the UAE, protect yourself first.

Keep 3–6 months of expenses in an accessible account as your emergency fund. This is the money that stays liquid — for job changes, medical surprises, or family needs.

Everything above that threshold is investable surplus. This is the money that should be working for you.

This single distinction resolves the emergency fund vs investing dilemma most expats struggle with: it’s not either/or. The emergency fund buys you security; the surplus buys you freedom.

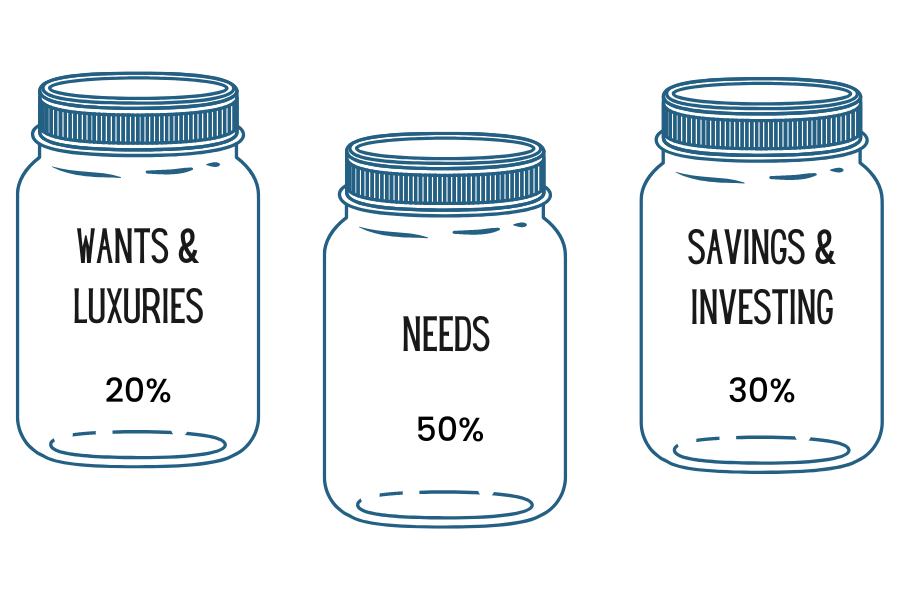

Step 2: Start With the EAB — The Expat Advantage Budget

The Expat Advantage Budget (EAB) is a practical, powerful tool I built for UAE residents to:

- ✅ Plan cashflow for the next 12 months in AED

- ✅ Break expenses into Needs, Wants, Savings, and Luxuries

- ✅ See your money in 8 currencies (INR, USD, GBP, EUR, CAD, SAR, OMR, SGD)

- ✅ Forecast potential wealth accumulation over 10, 15, or 20 years at 8% annual growth

📥 Click here to download the EAB (Excel or Google Sheet)

It’s free — and it’s the first step in taking charge of your money.

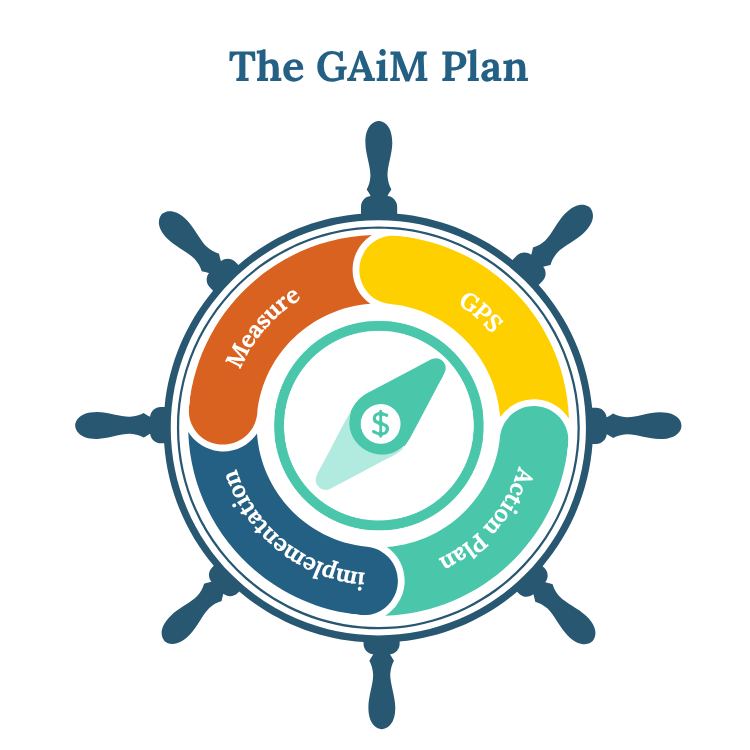

Step 3: Give Every Dirham a Purpose With the GAiM Plan

The GAiM Plan is a framework I developed to help UAE expats stop drifting and start building.

GAiM stands for:

- Goal Positioning System – Define your current financial situation and future goals clearly

- Action Plan – Align your income and surplus with a smart strategy

- implementation – Start with the right tools and guidance

- Measure & Manage – Review regularly and realign as life evolves

The GAiM Plan isn’t about being perfect — it’s about being intentional.

It takes you from “I’m saving for something” to “I’m building wealth for life.”

Think beyond next year. Visualize retirement, your children’s education, homeownership, or financial independence — then assign your savings to those goals.

Step 4: Stay Invested — Don’t Park, Don’t Panic

Once your savings are invested with purpose, the job isn’t watching markets daily. It’s staying the course and reviewing your plan at least twice a year.

When you stop restarting your savings and start growing your investments, you change your entire financial trajectory.

Ready to go deeper on the investing side? Read my complete guide on how to build wealth in Dubai.

Frequently Asked Questions

How much money should I keep in my bank account in the UAE?

Keep 3–6 months of living expenses as an emergency fund in an accessible account. Anything beyond that is surplus that could be invested toward your long-term goals. Holding 10–20x your monthly salary in a current account means inflation is silently eroding your wealth.

Is it bad to keep all my savings in a savings account?

It’s not bad — it’s just expensive. UAE bank accounts typically pay little to no interest, while inflation reduces your purchasing power every year. Money sitting in your bank account beyond your emergency fund is a missed opportunity, not a safety strategy.

Should I build an emergency fund or start investing first?

Both — in sequence. Build your 3–6 month emergency fund first, then direct your monthly surplus into investments. The emergency fund protects your investments from being sold at the wrong time when life happens.

Where should I invest my savings in the UAE as an expat?

It depends on your goals, timeline, and risk profile — which is exactly why a plan comes before products. Common options for UAE expats include globally diversified index funds and ETFs, retirement-focused investment plans, and goal-based portfolios. A structured framework like the GAiM Plan helps you choose with clarity instead of guesswork.

Final Thought: Your Future Self Will Thank You

Money sitting in your bank account isn’t bad — but it’s not building wealth either.

And money without a plan almost always ends up funding lifestyle upgrades or missed opportunities.

So the next time you look at your savings, ask yourself:

“Is this money just waiting to be spent… or is it fueling my future?”

👋 Let’s Take the First Step Together

If you’re ready to move beyond short-term saving and decide what to do with your savings — with clarity and confidence — I’d love to help.