Best Investments in UAE: The Complete (2026) Guide

Simple, efficient investment solutions to help you grow your wealth, create passive income, and reach your financial goals faster.

Expats are drawn to the UAE for its booming economy, tax-free personal income, and the chance to build wealth faster than almost anywhere else. Beyond the lifestyle, the country offers a genuinely diverse range of investment options; from real estate and global stocks to mutual funds, ETFs, bonds, and portable retirement and education plans — all in one of the most tax-efficient environments in the world.

This guide walks you through the best investments in the UAE for expats in 2026: why to invest, the main asset classes and how they work, the three stages of building wealth, and how to choose the right advisor to put it all together.

Table of Contents

4 Reasons to Invest Your Savings in the UAE?

Leaving your surplus cash in a bank account feels safe, but it quietly loses value to inflation every year. Investing puts that money to work. By investing in the UAE you can:

- Achieve financial independence — build investments that generate dependable passive income to support your lifestyle.

- Combat inflation — protect your purchasing power instead of watching it erode in a low-interest account.

- Reach long-term goals faster — fund retirement, children’s education, or a home purchase more efficiently.

- Create generational wealth — secure not just your future, but your family’s.

“The best time to plant a tree was 20 years ago. The second-best time is now.” — Chinese proverb

Best Investment Options in the UAE

The UAE and Dubai impose no capital gains or income tax on investment returns for individuals, making almost every asset class more rewarding here than in most home countries. Here are the main options expats use to build wealth.

Real Estate

Property is the best-known route to building wealth and passive income in the UAE. Foreign nationals can buy with full ownership rights in designated freehold areas, and gross residential rental yields averaged around 5.45% across the UAE in late 2025 — with Dubai apartments reaching as high as 7%. Property worth at least AED 750,000 can also qualify you for a renewable residency visa, and AED 2 million+ for a ten-year Golden Visa. The trade-off is that property is capital-intensive and less liquid than other assets. (For income strategies, see my guide to passive income in UAE.)

Stocks

UAE residents have easy access to far more than just local markets. Locally, you can trade on the Dubai Financial Market (DFM), Abu Dhabi Securities Exchange (ADX), and Nasdaq Dubai.

More importantly, regulated UAE platforms and international brokers give you direct access to the world’s largest equity markets — US stocks (NYSE, NASDAQ) for global tech and growth leaders, Indian stocks (NSE, BSE) for one of the world’s fastest-growing economies, and major European exchanges (London, Frankfurt, Paris) for blue-chip dividend payers.

You earn both dividend income and tax-free capital gains, and you can spread your portfolio across currencies and economies to manage country risk. Stocks offer strong long-term growth but carry real volatility, so research or professional guidance matters.

Mutual Funds

Mutual funds pool money from many investors into a professionally managed, diversified portfolio. UAE residents can access both locally registered funds — over 30 are domiciled with the Securities and Commodities Authority (SCA) — and a vast universe of international mutual funds from global asset managers like BlackRock, Fidelity, JP Morgan, and Franklin Templeton, covering US, European, Indian, emerging-market, and global thematic strategies.

AED- and USD-denominated options are widely available. You can invest a lump sum or set up a regular monthly plan (SIP), making funds one of the most practical, hands-off ways for busy expats to build a diversified portfolio. Watch the fees, as charges directly reduce your returns.

Exchange-Traded Funds (ETFs)

ETFs are pooled funds you can buy and sell on an exchange throughout the trading day, usually tracking an index rather than trying to beat it. They typically cost less than actively managed mutual funds and disclose their holdings publicly. They’re a low-cost, transparent core for many portfolios.

Bonds and Sukuk

ETFs are pooled funds you can buy and sell on an exchange throughout the trading day, usually tracking an index rather than trying to beat it. From the UAE you can access globally listed ETFs covering the S&P 500, Nasdaq 100, MSCI World, FTSE India, European indices, and specialist sectors and themes, typically at far lower cost than actively managed mutual funds, with full public disclosure of holdings. For many expats, a small handful of broad-market ETFs forms the low-cost core of a global portfolio.

Gold

Gold is a classic safe-haven asset that tends to hold or gain value during downturns and inflation. In Dubai you can buy physical bullion, gold ETFs, gold mutual funds, or shares in mining companies. It adds balance to a portfolio, though it generates no income on its own.

Portable Plans for Expats

Because expat life is mobile, portable retirement and education savings plans — ones you can keep contributing to and take with you when you leave the UAE — are among the most valuable tools available. They turn irregular expat careers into a structured path toward a specific goal.

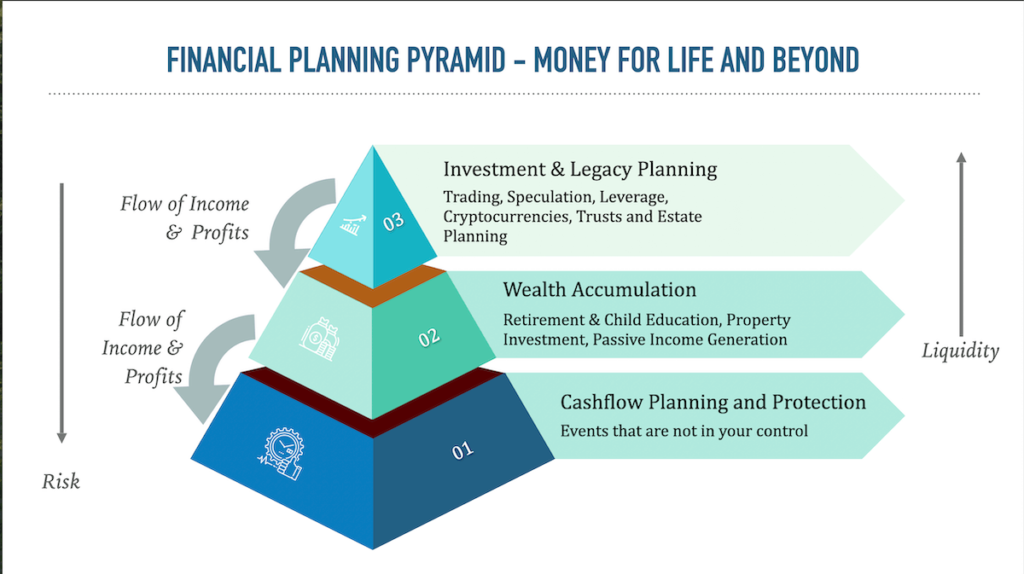

The 3 Stages of Building Wealth

People start investing at different ages and life stages. The Financial Planning Pyramid shows where you are and what to focus on next.

1. Foundation — building security. Save 3–6 months of expenses in cash or near-cash (National Bonds, deposits), clear high-interest debt like credit cards, and put adequate life and critical illness cover in place to protect your income.

2. Growth — building wealth. With the foundation set, focus on accumulation for big goals — retirement, education, property. Invest in mutual funds, ETFs, and stocks, diversify to manage risk, and consider real estate for income and appreciation.

3. Preservation — securing generational wealth. Shift toward steady income (dividends, annuities) and plan for wealth transfer with estate planning and insurance, so your wealth lasts beyond your lifetime.

Each stage builds on the one before, moving you closer to financial independence.

👉 Not sure which stage you’re in?

A free GAiM Plan discovery call maps exactly where you stand and what to do next. Book My Free Discovery Call →

Investing for Passive Income

One of the most common reasons expats invest is to build income that doesn’t depend on their salary. Rental property, dividend-paying stocks and funds, bonds, and annuities can all generate regular cashflow. Because this is a big topic in its own right, I’ve covered the strategies, current yields, and how to start in a dedicated guide: Passive Income in UAE: 8 Proven Ways to Earn in 2026.

The GAiM Plan: How I Help You Invest

Knowing the options is one thing; building and managing a portfolio that actually reaches your goals is another. As an independent financial advisor in Dubai, my job is to understand your objectives, horizon, risk tolerance, and cashflows — then recommend the right solutions, free of any product-push agenda.

I do this through the GAiM Plan, a four-step planning, advisory, and portfolio-management system:

- Goal Positioning System (GPS) — know exactly where you stand and where you want to go.

- Action Plan — a clear, step-by-step path to your goals, so the next move is always obvious.

- Implementation — putting the plan to work, beating the analysis-paralysis that stalls most people.

- Measuring Progress — regular reviews and adjustments to keep you on track.

We repeat this cycle until your goals are met.

How to Choose a Financial Advisor in UAE

The UAE advisory market is crowded, and not all advice is equal. A few things to look for:

- Independence. An independent advisor can recommend across the whole market; a tied agent can only sell their own firm’s products.

- Fee transparency. Understand exactly how your advisor is paid and what you’re paying for.

- Qualifications and track record. Look for recognised credentials and genuine local experience.

- A planning-first approach. The right advisor starts with your goals, not a product.

For context, I hold a Cert CII qualification with 14+ years advising expats in the Dubai market, and every recommendation runs through the GAiM Plan framework above.

👉 Ready to build your investment plan?

Book a free, no-obligation GAiM Plan consultation and let’s design an investment strategy built around your goals. Book My Free Consultation →

More on Investing

Explore my most-read guides:

- Passive Income in UAE: 8 Proven Ways to Earn

- How to Invest in UAE Using the 3-Bucket Approach

- The 5Cs Blueprint for Investing in the UAE

- 5 Rules for Successful Investing

- Mutual Funds in UAE: How to Build a Robust Portfolio

Frequently Asked Questions

What are the best investments in the UAE for expats?

The most popular options are real estate, stocks, mutual funds, ETFs, bonds and sukuk, and gold, alongside portable retirement and education plans. The best mix depends on your goals, time horizon, and risk tolerance — most diversified portfolios combine several.

Can expats and non-residents invest in the UAE?

Yes. Expats can invest in nearly all UAE asset classes, and non-residents can buy stocks, freehold property, and many funds. You’ll typically need valid ID and to complete a KYC process with a licensed provider.

How do I start investing in the UAE?

Define your goals and time horizon, decide your risk tolerance, build an emergency fund first, then choose assets that fit — using a Regular savings or Lump sum investment plans through Central bank, SCA- or DFSA-regulated platforms. Many people work with an independent advisor to structure this properly.

Is investment income taxed in the UAE?

For individuals there is no personal income, capital gains, or dividend tax in the UAE, so investment returns are generally tax-free for residents. If you have tax obligations in another country, those may still apply.

What is the minimum amount needed to start investing?

The minimum amount depends on the type of investment. You can start small, for lump-sum investment the minimum is $32,500 and for regular savings the minimum is $500.

You can buy life and critical illness insurance starting as low as $50 a month.

How do I choose a financial advisor in the UAE?

Favour independent advisors who can recommend across the whole market, are transparent about fees, hold recognised qualifications, and start from your goals rather than a product.

How much of my income should I invest?

A general rule of thumb is to save and invest at least 30% of your income, but this varies based on your financial goals and expenses. Click here to Supercharge Your Savings and Investments with the Expat Advantage Budget(EAB).

Which is better lump-sum and regular savings investments?

Lump-sum investments involve a one-time large amount, suitable for long-term wealth growth. It is ideal when investing for long term goals in favorable market conditions

SIP / Regular savings plans involve smaller, periodic contributions, ideal for building wealth over time. SIPs are ideal for any market condition.

Take the Next Step

The hardest part of investing isn’t picking products; it’s putting a plan together that fits your goals, timeline, and risk profile, and then sticking to it through the market cycles.

That’s exactly what the GAiM Plan is built for. In one free 15-minute Discovery Call, we’ll:

- Get clear on your goals, priorities, and current situation.

- Find out how the GAiM Plan could work for you.

- Decide if you’d like to move to a Holistic Financial Planning Session.

No product pitch, no pressure. Just a clear view of what’s possible.

👉 Book Your Free GAiM Plan Discovery Call

15 minutes. Online. Walk away with clarity on your next move. Book My Free Discovery Call →