Passive Income in UAE: 8 Proven Ways to Earn in 2026

Building passive income in UAE is one of the smartest moves an expat can make. With no personal income tax, a stable Dirham pegged to the US dollar, and one of the world’s most active property and capital markets, the UAE gives you a genuine head start most people back home will never have.

But here’s the catch: your salary stops the day you stop working — or worse, the day you can’t. Passive income is what keeps cash flowing when your active income doesn’t. As Robert Kiyosaki put it, the real skill of the wealthy is converting earned income into passive and portfolio income.

This guide walks through eight proven ways to earn passive income in Dubai and across the UAE in 2026, what each realistically pays today, and how to start — whatever your budget.

What Is Passive Income? The Meaning, Explained

The meaning of passive income is simple: it is regular cash flow from assets you own or control that requires little ongoing effort once it’s set up. That’s what sets it apart from the other two ways money reaches you:

- Earned (active) income — salary, fees, profits. It’s tied directly to your time and stops when you do.

- Portfolio income — capital gains from buying an asset and selling it later at a higher price (property flips, trading shares).

- Passive income — recurring cashflow from rent, dividends, interest, or royalties.

The advantage of passive income is simple: once established, it keeps paying for the foreseeable future, and good sources (like rent) tend to grow with inflation. That makes it the engine of financial independence and a comfortable retirement.

8 Ways to Earn Passive Income in UAE in 2026

1. Rental Income From UAE Property

Real estate remains the most popular route to passive income in Dubai — and 2026 numbers explain why. Gross residential rental yields in the UAE averaged around 5.45% in late 2025, up from roughly 4.9% a year earlier, with Dubai apartments reaching as high as 7% gross in stronger communities. Affordable, high-demand areas such as JVC, Discovery Gardens, and Dubai South can push gross yields into the 8%+ range.

A simple example: buy an apartment for AED 1,000,000 that rents for AED 70,000 a year and your gross yield is 7%. Just remember to work in service charges and maintenance to get your net yield — in luxury towers these costs are far higher than in budget communities.

Property is also where most expats need the most planning. Buying off-plan or with a mortgage means juggling down payments, construction-linked instalments, and monthly repayments against your rental income and salary. Getting that cashflow wrong is what turns a good investment into a stressful one. A big part of what I do is help clients set clear property investment goals and build a plan to fund the mortgage and off-plan payments without straining the rest of their finances — so the asset works for you, not the other way round.

Best for: Investors with capital for a down payment who want an inflation-linked, tangible income stream.

2. Fractional Property Ownership — Real Estate From a Few Hundred Dirhams

Don’t have AED 200,000+ for a property deposit? Fractional ownership lets several investors collectively own a single property, each holding a percentage stake and receiving a matching share of the rental income — often paid monthly. DFSA-regulated platforms in Dubai now let you start from as little as AED 500, making this one of the lowest-entry ways to earn property income in the UAE. You get rental cashflow and exposure to property price growth without the large capital, mortgage, or management hassle of buying outright.

Best for: Anyone who wants property income but doesn’t have the capital for a full down payment.

3. Dividend-Paying Stocks

Shares in established, profitable companies pay out a portion of earnings as dividends — cash that lands in your account whether the market is up or down. UAE-listed companies on the DFM and ADX have a strong dividend culture, and you can diversify globally into US, European, and Canadian dividend payers for currency and sector spread.

Best for: Growth-stage investors who want a blend of rising capital value and a regular cash payout.

4. Dividend-Paying Mutual Funds

If picking individual dividend stocks feels like too much work or risk, dividend-focused mutual funds do it for you. A professional manager builds a diversified basket of income-paying companies — often across multiple countries and sectors — and distributes the income to you, typically monthly, quarterly, or annually. You get instant diversification and hands-off management from a single investment, which makes these funds one of the most practical income tools for busy expats. Watch the fund’s charges, as fees eat directly into your yield.

Best for: Investors who want regular, diversified dividend income without researching and managing individual shares.

5. Bonds and Sukuk

Bonds (and their Sharia-compliant equivalent, sukuk) pay you fixed, predictable income in return for lending your capital. The UAE Federal Government and the Dubai and Abu Dhabi governments all issue sovereign sukuk, and products like National Bonds’ Term Sukuk let you start from as little as AED 10,000 with capital protection and regular profit distributions.

Best for: Conservative investors who prioritise capital safety and steady, dependable cashflow.

6. Fixed Deposits and High-Yield Savings

The simplest passive income of all — and entirely tax-free for UAE residents. With the CBUAE base rate held at 3.65% in early 2026, the best fixed deposits were paying up to around 4.25–4.75% p.a. depending on tenure and bank. It won’t make you rich, and it may barely beat inflation, but it’s the right home for your emergency fund and short-term cash.

Best for: Your 3–6 month emergency buffer and money you can’t afford to risk.

7. Annuities and Pension Plans

Annuities and structured pension plans convert a lump sum or regular savings into a guaranteed income stream — often for life. For expats with no employer pension, a portable retirement plan you can take with you when you leave the UAE is one of the most reliable ways to manufacture a salary in retirement.

Best for: Anyone serious about replacing their paycheck once they stop working.

8. Royalties and Digital Assets

Intellectual property — books, music, courses, photography, software — can pay royalties for years after the work is done. It takes real effort upfront, but few income streams are as genuinely “passive” once they’re live.

Best for: Professionals and creators who can package their expertise once and sell it repeatedly.

The Real Challenges (And How to Beat Them)

Most expats know they should build passive income. Three things usually stop them:

- Not enough capital. Many income assets need a meaningful lump sum to generate meaningful income.

- Not enough knowledge or time. Building and managing a diversified portfolio is a skill, and markets move fast.

- No dependable advice. The UAE advisory market is crowded with product-pushers, making trustworthy guidance hard to find.

The solution to all three starts in the same place: capital accumulation. You need a critical mass of investable capital before passive income becomes significant — and the most efficient way to build it is disciplined saving from your active income, invested consistently and early.

Not sure where to start, or which mix is right for your situation? My GAiM Plan consultation walks you through it, free.

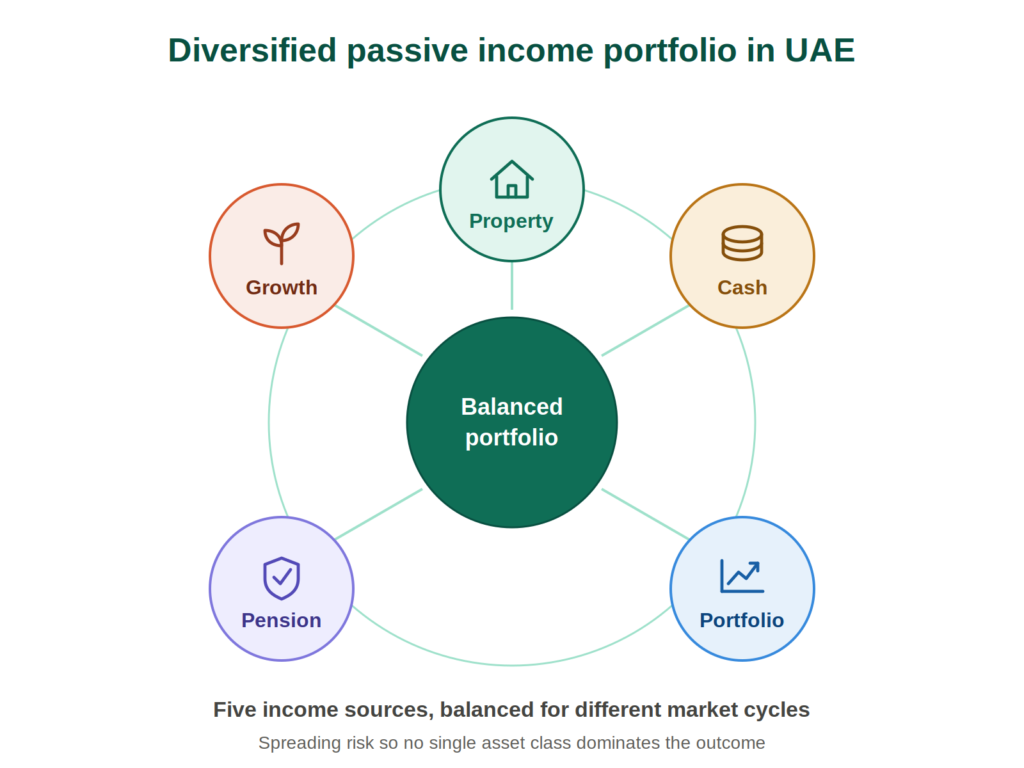

Case Study: Why One or Two Income Streams Isn’t Enough

A point worth stressing: relying on just one or two sources of passive income is a risk in itself. Markets move in cycles, and an asset that looks dependable today can underperform for years when the cycle turns. The defence is diversification across asset classes that don’t all rise and fall together.

I recently worked with a couple who wanted exactly this — passive income they could count on through good markets and bad. Rather than concentrating their wealth in property alone, we built a plan across five complementary asset classes:

- Property — for inflation-linked rental income and long-term capital growth.

- Cash — a liquid buffer for security and to seize opportunities when markets dip.

- An investment portfolio — a diversified blend of dividend-paying stocks, bonds, and mutual funds generating regular income.

- A guaranteed pension plan — a contractually secure income stream they can rely on regardless of market conditions.

- Growth stocks — a measured allocation to higher-growth equities to keep their wealth ahead of inflation over time.

The logic is simple: when one asset class has a weak year, the others keep the income flowing. No single adverse market cycle can derail the whole plan. That balance — between safety, income, and growth — is the heart of building passive income that genuinely lasts.

How to Start Building Passive Income in UAE

You don’t need to do everything at once. A sensible sequence:

- Secure the foundation — 3–6 months of expenses in a fixed deposit or National Bonds before anything else.

- Match the asset to your goal — bonds and sukuk for safety, dividends and funds for growth, property (full or fractional) for scale.

- Diversify — spread across asset types so one bad year doesn’t sink your income.

- Invest consistently — regular contributions plus the power of compounding do the heavy lifting over time.

- Review regularly — rebalance as markets and your life change.

Build Your Passive Income Plan With the GAiM Plan

Knowing the options is the easy part. Turning them into a reliable income stream that actually replaces your salary takes a structured plan — not a one-off product sale. That’s what the GAiM Plan is built for.

It’s the same four-step system I use with every client to design passive income that fits their numbers:

- Goal Positioning System (GPS) — we map exactly where you stand today and how much passive income you’ll need to be financially independent.

- Action Plan — a clear, step-by-step path that matches the right assets (rent, fractional property, dividends, sukuk, annuities) to your goals, budget, and risk profile.

- Implementation — we put the plan to work using the right platforms and strategies, so analysis paralysis never stalls you.

- Measuring Progress — regular reviews and rebalancing keep your income on track as markets and your life change.

As an independent advisor in Dubai with a Cert CII qualification and 14+ years in the UAE market, I work for your plan — not a product shelf.

👉 Get Your Free Passive Income Plan

Book a free, no-obligation GAiM Plan consultation and I’ll help you design a passive income strategy tailored to your goals, budget, and timeline.

Frequently Asked Questions

What is the meaning of passive income?

Passive income means earnings from an asset you own or control — such as rent, dividends, interest, or royalties — that keep coming in with little ongoing effort once set up. It contrasts with active income (your salary), which stops the moment you stop working.

How can I make passive income in UAE?

The most common ways are rental property, fractional property ownership, dividend-paying stocks, dividend-paying mutual funds, bonds and sukuk, fixed deposits, annuities, and royalties. The best route depends on your available capital, risk tolerance, and time horizon — most investors combine two or three.

What is the best passive income in UAE?

There’s no single “best” — it depends on your situation. Rental and fractional property offer inflation-linked income; dividends and funds balance growth and cashflow; sukuk and fixed deposits offer safety. A diversified mix usually beats relying on any one source.

How much money do I need to start earning passive income in Dubai?

You can start small — fixed deposits and some sukuk products accept from AED 5,000–10,000, and fractional property platforms let you access property income from as little as AED 500. Buying a physical property outright typically requires a deposit of around 20–25% of the purchase price.

Is passive income taxable in the UAE?

For individuals, there is no personal income tax in the UAE, so rental income, dividends, interest, and capital gains earned by residents are generally tax-free. Always confirm your own position, especially if you have tax obligations in another country.

How much passive income do I need to be financially independent?

Enough to cover your annual living expenses from investments alone. As a rough guide, many planners target investments worth roughly 25 times your yearly spending — but the right number is personal, which is exactly what a financial plan is for.

Book a free, no-obligation GAiM Plan consultation and I’ll help you design a passive income strategy tailored to your goals, budget, and timeline.