Retirement Planning After 50: A Smart Catch-Up Guide

Is 50 too late to start retirement planning?

Not really!

If you’re 50 years old or older and concerned that it’s too late for you, it’s highly likely that it isn’t.

The years between 50 and retirement are often the most powerful saving window of your entire life — your income is peaking, your big expenses are winding down, and you finally have the clarity to make decisions that count. The trick is to move deliberately, not anxiously.

This guide shows you exactly how to catch up with your retirement planning after 50 — what steps to follow, in what order, and which mistakes to avoid.

Why 50 Is a Stronger Starting Point Than You Think

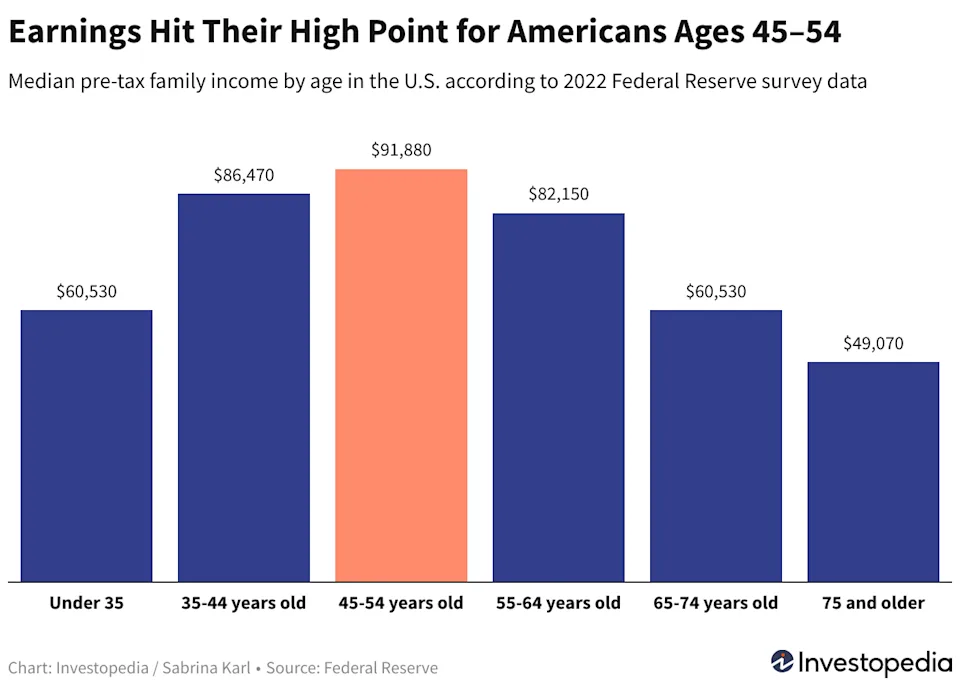

Most people hit their peak earning years in their early-to-mid fifties. By this stage, the heavy lifting of your earlier decades is usually behind you.

Children are often finished with college and standing on their own feet.

Major goals — buying a home, building a business, the big travel — have either been achieved or scaled back. The mortgage may be smaller or gone. The result is a combination you rarely have when you’re younger: higher income and lower expenses at the same time.

That gap between what you earn and what you spend is the engine of catch-up retirement saving. More income and fewer obligations is, quite simply, an excellent recipe for building a retirement fund quickly.

How to Save for Retirement After 50: A Step-by-Step Plan

You don’t need a complicated strategy. You need a focused one. Here are the seven steps that matter most.

1. Take an honest financial inventory

Start with a clear picture of where you stand today: total savings and investments, any outstanding debt, monthly income, and monthly spending.

You cannot plan a route without knowing your starting point.

Be precise rather than optimistic — this number is the foundation for everything that follows.

2. Define what retirement actually looks like for you

Decide the lifestyle you want, the age you’d like to stop working, where you intend to live, and any large future costs.

A retirement in a low-cost city looks very different from one in a major financial hub, and your target number should reflect that. Put a figure on it, even a rough one — a goal you can measure is a goal you can hit.

3. Maximise your contributions

This is where catch-up planning earns its name. Push your savings rate as high as you comfortably can. If your employer offers a pension or savings scheme, contribute enough to capture the full benefit. If you already have a personal investment plan, increase the contributions.

If you don’t have one, this is the time to start. With a shorter runway, your savings rate does more work than market returns.

4. Protect the plan with the right insurance

A retirement plan is only as strong as your ability to keep funding it. A serious illness in your fifties can force you to retire earlier than planned — and the data backs this up: the average age for critical illness claims in this market sits around the late forties to early fifties. Adequate life and critical illness cover means an unexpected diagnosis doesn’t derail decades of saving. Review what you have, identify the gap, and close it.

5. Clear debt and build emergency savings

High-interest debt quietly drains the money that should be compounding for your future. Prioritise paying it down. At the same time, keep an emergency fund of several months’ expenses so that a surprise cost doesn’t force you to sell investments at the wrong moment.

6. Sort out your estate and legacy

Make sure your assets pass to the people you intend, in the way you intend. This means a valid will and, where appropriate, trust structures. Inheritance rules can vary significantly depending on your residency and faith, so get specific advice rather than assuming. Talk openly with your family about your plans — clarity now prevents disputes later.

7. Review, adjust, repeat

Your plan is not a document you write once and file away. Markets shift, income changes, and goals evolve. Revisit the plan at least once a year and adjust contributions, allocations, and timelines as your circumstances change.

What is the best investment for retirement after 50?

Saving builds the nest egg; investing protects it from inflation and currency erosion. When your time horizon is shorter, the characteristics of an investment matter even more. Here’s what to prioritise.

Alignment with your goals and risk appetite. Your investments should match your timeline, income needs, and tolerance for ups and downs. As retirement approaches, a more measured approach helps protect what you’ve built.

Flexibility, not a long lock-in. Catching up means committing a meaningful chunk of savings — but that money should stay flexible. Avoid rigid, long-term contractual products that penalise you heavily if your income or residency changes. You want options, not handcuffs.

Stable, reliable returns. Chase consistency over headline-grabbing volatility. And learn the difference between risk and volatility: avoid genuine risk, but treat market volatility as something you can use, not fear.

Inflation protection. Your money needs to grow faster than prices rise, or its purchasing power quietly shrinks. Equities, funds, ETFs, real estate, and inflation-linked assets all help here.

Diversification. Spread across asset classes, sectors, and regions so that no single setback can sink the plan.

Liquidity. Keep reasonable access to your money, especially as you near retirement, without steep penalties.

Low fees. High charges compound against you just as returns compound for you. Favour low-cost options — the difference over a decade is substantial.

Tax and currency efficiency. Consider tax implications both where you live and back home, and account for exchange-rate risk if you hold money in more than one currency. For many expats, a stable, dollar-based plan reduces this risk meaningfully.

Transparency. Insist on understanding every charge and term before you commit. If an advisor can’t explain the costs clearly, that’s your answer.

A Note for Expats and NRIs

If you’re an expatriate, your fifties carry an extra layer of planning. Employer end-of-service benefits are rarely enough to fund a full retirement on their own, and they aren’t a substitute for a personal investment plan. Currency exposure matters more when your future spending may happen in a different currency than your savings. And cross-border tax and estate rules can complicate an otherwise simple plan. These aren’t reasons to worry — they’re reasons to plan with someone who understands the expat picture specifically.

Frequently Asked Questions

Is 50 too late to start saving for retirement?

No. The years from 50 to retirement are often your highest-earning, lowest-expense period, which makes them ideal for aggressive catch-up saving. A focused plan started at 50 can still build a substantial fund.

How much should I save for retirement if I start at 50?

There’s no single figure — it depends on your target retirement age, the lifestyle you want, and your existing savings. The practical answer is to save as high a percentage of income as you comfortably can, because at this stage your savings rate matters more than expected returns.

What’s the best way to invest for retirement after 50?

Prioritise diversified, flexible, low-cost investments with stable returns and good liquidity, aligned to your timeline and risk tolerance. Avoid long, rigid lock-ins, and protect the plan with adequate critical illness and life cover.

Should I take less risk as I get closer to retirement?

Generally, yes — a more measured allocation protects what you’ve built. But don’t confuse short-term volatility with permanent risk; some growth exposure usually still makes sense to outpace inflation through a retirement that may last decades.

Start Now — It’s Not Too Late

Reaching 50 isn’t a deadline you’ve missed. It’s a window that’s wide open. You have the experience, the income, and the clarity to make genuinely smart choices for your future. The only thing left is to begin.

Book a free Discovery Call and let’s build a retirement plan that fits your timeline, your goals, and your life.