Life Insurance for Women in the UAE: Why Most Get It Wrong

Most women in the UAE are either underinsured or worse, completely uninsured.

Homemakers especially and even women with stable careers and strong salaries

Not because they can’t afford it; but because they don’t feel the need for it.

If income is lower than their partner’s, it feels less important.

And if there is no income, it feels unnecessary.

So life insurance for women gets delayed or worse ignored…

The reality is, whether income is visible or not, the financial impact is real.

While a working woman supports the household directly; a homemaker supports it in ways that would be expensive to replace; childcare, home management, stability.

If either role is disrupted, the impact is immediate and significant.

By the time the need feels real, it is often too late.

Life Insurance for Women: 5 Mistakes to avoid.

1. Thinking Homemakers Don’t Need Cover

This is one of the biggest blind spots.

A homemaker may not bring in an income but her contribution to the household is indispensable. Childcare, household management, and the daily stability that holds a family together, these are not small things. They are the foundation the entire household runs on.

If something happens to her, that foundation cracks. The responsibilities don’t pause for grief. They show up the next morning and every morning after.

In the UAE, this reality hits harder than most places.

The majority of expat families here are nuclear; There are no grandparents nearby, no extended family stepping in. Each parent is load-bearing. When one is gone, there is no safety net waiting in the next room. There is just the gap and the cost of filling it.

That cost is real.

Childcare, household help, school runs, meals and coordination; in Dubai, replacing what a homemaker provides can run into thousands of dirhams a month.

Yet because there is no salary attached to it, most families never think to insure it.

A homemaker’s value was never invisible. It was just never counted until it has to be replaced.

2. Assuming Lower Income Means Lower Risk

Many women underestimate their financial contribution, especially if they earn less than their partner.

But the real question is not:

👉 Who earns more?

It’s: 👉 What breaks if this income stops?

Working couples build their financial lives on a quiet assumption that both incomes will continue, month after month, until retirement.

That assumption shapes everything: the apartment they chose, the school they committed to, the Education savings plan they started, the goals they set together.

When one income stops; even the smaller one that assumption collapses.

Savings slow down or stop entirely. Investments get paused. Lifestyle scales back.

And if the gap is wide enough, the family starts borrowing to stay afloat, or falls behind on payments they never expected to miss.

And that is just the financial damage.

What rarely gets spoken about is the weight that lands on the surviving partner. They are now the sole earner, the sole parent, and the sole decision-maker all at once. The stress of bridging the income gap does not arrive separately from the grief. It arrives at the same time.

Life insurance is not sized by who earns more. It is sized by what would break without you.

And for most women in dual-income households, the honest answer to that question is: quite a lot.

3. Just Relying on Employer Cover

Most women assume they’re covered because their employer provides life insurance. It feels like a box ticked; something in place, something to point to.

But employer cover is not a financial plan. It is a starting point — and a very small one

Here is what employer-provided life insurance typically looks like:

- Limited — usually 2–3x your basic annual salary. Enough to cover a few months of expenses, not years of financial obligations

- Temporary — it exists for as long as you stay in that job. Change roles, resign, get made redundant, or take a career break, and it is gone. No warning, no replacement

- Generic — designed around a standard employee profile, not around your mortgage, your children’s school fees, your family’s actual cost of living, or your partner’s dependence on your income

In the UAE, this problem is sharper than most people realise.

Expat careers are mobile by nature. Job changes are common. Career breaks for family especially among women happen more than the industry acknowledges.

Every time your employment status shifts, so does your cover. Most people only discover this when it is too late to do anything about it.

Employer cover is better than nothing. But if your income supports your lifestyle or your family, “better than nothing” is not a plan.

Real cover is portable. It is sized around your life, not your job title. And it does not disappear the day you hand in your notice.

4. Delaying the Decision

“I know this is important, but I’ll do it later.”

Later is the most expensive word in financial planning.

Because while you wait, three things happen quietly against you:

- Premiums increase with age — the same cover costs significantly more every year you delay

- Health changes can make you uninsurable — a diagnosis, a flagged test result, a procedure. You cannot go back and buy yesterday’s health

- Responsibilities grow faster than protection — the school fees arrive before the policy does. The mortgage grows before the cover does

Life insurance works on a simple but ruthless logic. It is cheapest and easiest to get when you are young, healthy, and feel like you do not need it yet.

That feeling is exactly the right time to act.

Waiting until it feels urgent means the decision has already been made for you, nut just not in your favour.

5. Not Reviewing Cover as Life Changes

A policy taken out five or ten years ago was designed for the life you had then.

It does not account for the second child, the school fees that have doubled, or the lifestyle that quietly expanded as your income grew. Life has moved up. Your cover is still way back where you started.

Most people set up a policy and consider it done. Meanwhile, everything it was supposed to protect has changed shape.

Marriage. A growing family. A bigger home. A career jump. Each one increased what your family depends on. None of them automatically updated your cover.

The rule is simple — every major life event is a reason to review. Not because the old policy was wrong. Because your life outgrew it.

Outdated cover is not protection. It is a false sense of security with a policy number attached.

3 Risks Most Women Overlook

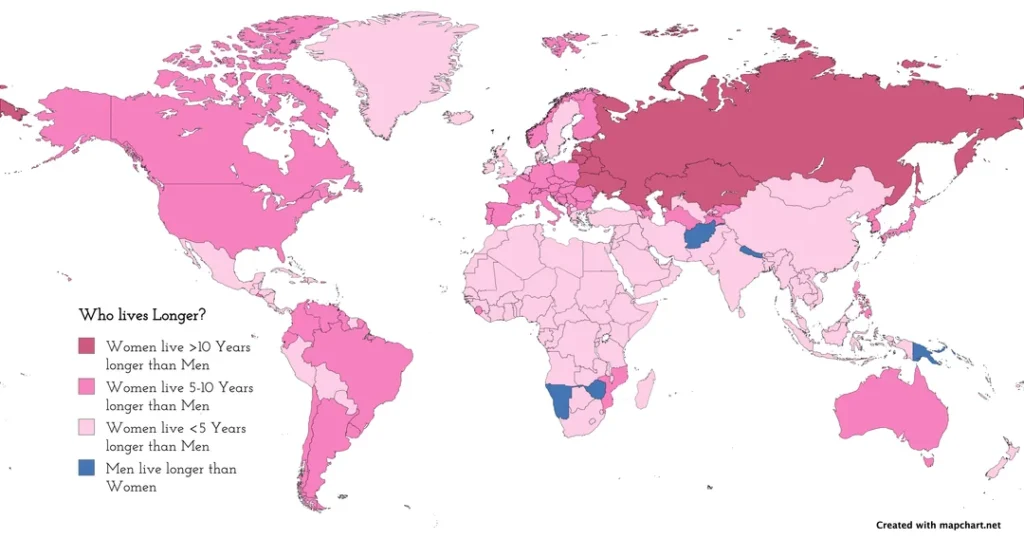

Longevity

Women statistically outlive men globally by an average of five years, often more.

That sounds like good news. In financial terms, it is a risk.

Living longer means funding a longer retirement. It means a higher chance of spending years sometimes decades as the sole financial decision-maker in the household.

It means needing savings, investments, and protection to stretch further than most plans account for.

A woman who outlives her partner does not just lose companionship. She loses a second income, often a pension, and sometimes the life cover that was supposed to protect her. If she was not insured in her own right, she is now exposed later in life, when rebuilding is hardest.

Longevity is not just a blessing. Without a plan, it is a liability.

And here is the irony.

Because women live longer, insurers consider them a lower mortality risk. That translates directly into lower premiums. The same cover, the same sum assured, the same policy term and a lady pays less for it than a man of the same age.

So the one group most likely to delay, most likely to feel it is unnecessary, and most likely to be underinsured is also the group that gets the best price.

The cover is more affordable. The need is just as real.

If cost was ever your excuse to delay or defer, it just ran out.

Critical Illness

Life insurance protects your family if you die. But what protects you and your family when you survive a major ailment?

A critical illness; cancer, a stroke, a heart condition does not always end a life.

But it can turn it upside down. Recovery takes time. Treatment costs in the UAE are significant even with health insurance. And while you are focused on getting better, the bills do not pause; the rent, the school fees, the EMIs, the life you built together.

This is where a critical illness benefit changes everything.

A lump sum paid on diagnosis gives you choices.

- The choice to step back from work without financial panic.

- The choice to access better treatment.

- The choice to focus entirely on your recovery, knowing your family’s financial foundation is still standing.

The data shows why this matters for women specifically. According to Zurich International Life’s Customer Claims Paid Report 2025,

- Heart attack and stroke-related death claims among women have risen by 50% since 2020.

- Of all women who made living benefit claims with Zurich, 4 out of 5 claimed for cancer making it by far the leading critical illness risk for women.

- And smoking, often underestimated as a risk factor, is actually more dangerous for women’s heart health than it is for men.

- Yet despite this, 3 out of 5 women insured with Zurich carry cover of less than $200,000 a sum that would not sustain most UAE expat families through a serious illness, let alone beyond it.

The right cover does not just protect against the worst. It gives you the freedom to heal, recover, and rebuild on your terms.

Career Breaks

Many women step back from work at some point for maternity, for childcare, for a family member who needs care, or simply to reset.

During that time, employer cover disappears. Income stops. And the window to build financial protection quietly closes.

Career breaks are often temporary. The financial vulnerability they create can last much longer. A woman who re-enters the workforce after a break may find premiums higher, cover harder to qualify for, and years of protection lost that cannot be recovered.

The time to get insured is before the break not after.

In Summary

The five mistakes in this blog are not about carelessness. They are about under estimation of the the risk and importance of income replacement. Or assuming that the employer policy is enough or that there will be a better time later.

Most of these assumptions feel reasonable. None of them hold up when they are tested.

Whether you are a homemaker, a working professional, a primary earner, or a second income your financial contribution is real, your risk is real, and your cover should reflect both.

A Final Word

Life insurance for women is not a niche product or a secondary conversation.

It is foundational financial planning and in the UAE, where most expat families are on their own without a wider safety net, it matters more than most places.

The best time to review your cover is before you need it. Before the career break. Before the diagnosis. Before the life event that changes everything.

If you are reading this and recognising yourself in any of these five mistakes, that recognition is the first step.

The next one is a conversation.