How to Budget Efficiently?: A 5 Steps Guide for Beginners

Wealth building is actually simple in theory.

It requires just three steps:

- Earn money

- Save money

- Invest money

The UAE offers tremendous opportunity for the first step. Many professionals earn tax-free income and have the potential to build significant wealth during their working years.

But this is where many people lose track.

They are constantly seeking to earn more.

They talk about investing.

Yet they overlook the most important step in between.

Saving.

Without structure, income quietly disappears into lifestyle upgrades, subscriptions, travel, and everyday spending.

Before investing can work, saving must become intentional and consistent.

This is where budgeting becomes critical.

Learning how to budget helps you convert income into long-term wealth.

In this guide, we will walk through how to create a budget step-by-step, along with practical budgeting methods, examples, and tips for beginners.

Table of Contents

What is Budgeting?

Budgeting is the process of planning how your income will be spent, saved, and invested.

Instead of wondering where your money went at the end of the month, a budget allows you to decide in advance how your money should work for you.

The objective of budgeting is not merely to make ends meet.

The real purpose is to create an investable surplus every month, so that your income gradually converts into long-term wealth.

A well-structured budget helps you:

• control spending

• save consistently

• avoid unnecessary debt

• reduce financial stress

• build long-term wealth

Budgeting is not about restricting your life.

It is about directing your money toward what matters most.

Why is Budgeting important?

A budget helps you do more with your money. With a budget, spending becomes intentional. Without one, it often becomes impulsive or worse, compulsive.

A well-structured budget helps you:

• build an emergency fund

• pay your bills on time and maintain a lifestyle that aligns with your income

• invest regularly

• eliminate debt faster( if any)

• prepare for retirement

• achieve long-term financial goals

Budgeting creates financial clarity, which is the foundation of long-term wealth.

How to Budget: Step-by-Step

Creating a budget is not complicated. It simply requires clarity and discipline.

Here is a practical step-by-step process for creating a budget.

Step 1 – Determine Your Monthly Income

To build an accurate budget, you must first understand your real monthly income.

Only include income that is consistent and reasonably predictable, such as:

• Salary, including average monthly commissions or allowances

• Annual bonus divided by 12 to estimate the monthly equivalent

• Regular business income

• Predictable rental income

• Passive income, such as interest, dividends, or other regular investment income

Convert all income sources into monthly figures to make budgeting easier.

Avoid relying on uncertain or irregular income when planning your core budget.

For better accuracy, review your last 12 months of bank statements and calculate the average monthly income.

This provides a realistic foundation for your budget and prevents overestimating how much you can safely spend.

Step 2 – Categorize Your Expenses

The next step in creating a budget is organizing your spending into clear categories.

A simple approach is dividing expenses into three groups.

Needs

Essential expenses required for daily living:

• rent or mortgage

• utilities

• groceries

• insurance

• transportation

Wants

Non-essential lifestyle spending such as:

• dining out

• entertainment

• travel

• gadgets

• subscriptions

Savings and Investments

Money allocated toward your future goals:

• emergency savings

• retirement investments

• children’s education

• long-term wealth accumulation

Tracking these categories helps you understand where your money is actually going each month.

Step 3 – List and Organize Debt

If you have outstanding debt, it must be included in your budget.

Examples include:

• credit cards

• personal loans

• car loans

• mortgages

List each debt along with its interest rate and monthly payment.

Two popular strategies can help eliminate debt efficiently.

Debt Avalanche

Prioritize debts with the highest interest rates first.

Debt Snowball

Pay off smaller debts first to gain quick psychological wins.

Both approaches work. The key is consistency.

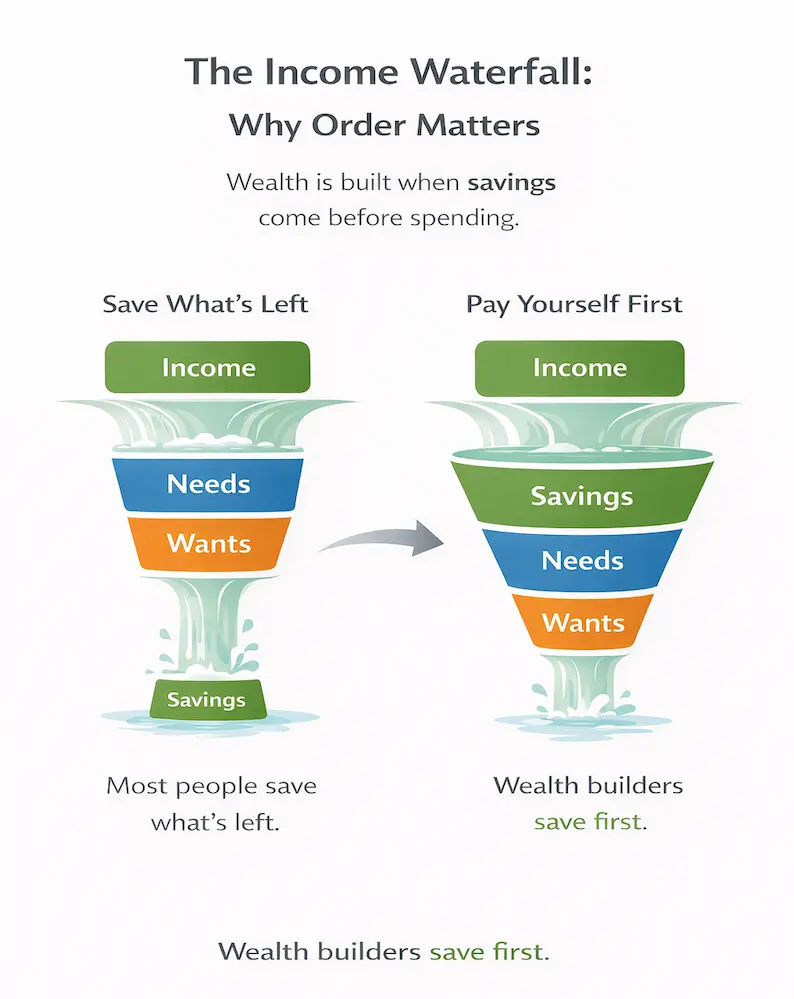

Step 4 – Define Your Savings Goals and Pay Yourself First

Once you understand your income, expenses, and debt obligations, the next step is to ensure that a portion of your income is consistently directed toward savings and investments.

This is often called the “Pay Yourself First” principle.

Instead of saving whatever remains at the end of the month, allocate a fixed percentage of your income toward savings as soon as you receive it.

A good starting point is 10–30% of your income. If that feels difficult initially, start smaller and gradually increase the percentage over time.

Your savings should also be linked to clear financial goals, such as:

• building an emergency fund

• retirement planning

• children’s education

• a property down payment

• future lifestyle goals

When savings are tied to meaningful goals, budgeting becomes far easier to maintain.

Automating savings through investment plans or systematic investment programs can also help build consistency and discipline.

Step 5 – Track and Review Your Budget

A budget is not a one-time exercise.

Your financial situation will evolve as income, family responsibilities, and goals change.

Review your budget at least once every month.

Ask yourself:

- Did I pay myself first?

- Did I overspend in any category?

- Can I reduce unnecessary expenses?

- Can I increase my savings rate?

Small adjustments made consistently can significantly improve financial outcomes over time.

Personal Budget Example

Here is a simple personal budget example using a commonly recommended budgeting framework.

| Category | Percentage | Example on $5,000 Income |

|---|---|---|

| Needs | 50% | $2,500 |

| Wants | 20% | $1,000 |

| Savings | 30% | $1,500 |

This structure helps balance current lifestyle needs with long-term wealth creation.

Popular Budgeting Methods

Several budgeting methods can help structure your finances.

Here are three of the most common approaches.

EAB – Expat Advantage Budget

The Expat Advantage Budget (EAB) is a budgeting framework designed specifically for expatriates, particularly those living in the UAE.

It helps you control spending, increase savings, and avoid the common trap of earning well but accumulating little wealth.

The EAB classifies expenses into three simple categories:

• Needs – essential living expenses such as rent, groceries, utilities, and insurance

• Wants – lifestyle spending such as dining, travel, and entertainment

• Savings – money directed toward emergency funds, investments, and long-term goals

The framework provides a clear 12-month overview of your income and expenses, making it easier to plan ahead and stay in control of your finances.

More importantly, it encourages you to maximize your savings potential while living in a tax-efficient environment like the UAE, helping convert income into long-term wealth.

50-30-20 Budget Rule

This simple budgeting method divides income into:

50% for needs

30% for wants

20% for savings and investments

It works well for beginners who want a straightforward budgeting system.

Zero-Based Budgeting

In this method, every dollar of income is assigned a purpose.

Income minus expenses minus savings equals zero.

This approach ensures every portion of income is intentionally allocated.

Pay Yourself First

This method prioritizes savings before spending.

Instead of saving what remains, savings are treated as the first expense.

This approach is widely used by successful investors.

Budgeting Tips That Actually Work

Many people start budgeting but fail to maintain it.

Here are practical budgeting tips that make the process easier.

Automate Your Savings

Automatic transfers remove the temptation to spend before saving.

Track Small Expenses

Daily spending like food delivery, subscriptions, and coffee can quietly consume large amounts over time.

Avoid Lifestyle Inflation

When income increases, direct part of that increase toward investments instead of upgrading every expense.

Involve Your Family

Budgeting works best when household members share financial goals.

Budgeting for UAE Residents and Expats

Budgeting is particularly important for expats living in the UAE.

Unlike many Western countries, UAE residents typically do not benefit from employer pension systems.

This means individuals must take responsibility for building their own long-term financial security.

A well-structured budget should therefore include:

• emergency savings

• long-term investments

• retirement planning

• protection through insurance

Without these elements, many professionals risk reaching retirement without adequate financial security.

Start Building Your Budget Today

Budgeting is the first step toward financial freedom.

Once you gain clarity over your income and spending, it becomes far easier to:

• increase savings

• invest consistently

• achieve long-term financial goals

If you want a practical way to get started, you can use the Expat Advantage Budget (EAB) — a simple tool designed specifically for UAE residents to track income, organize expenses, and build wealth systematically.

You can also book a discovery call to review your current financial structure and identify opportunities to improve savings and long-term investment planning.

If you want, I can also show you 3 small SEO tweaks that could push this article into the top rankings much faster(most people miss these, but they make a big difference).

How do beginners start budgeting?

Beginners can start budgeting by listing their monthly income, categorizing expenses into needs and wants, allocating money toward savings, and tracking spending each month.

What is the easiest budgeting method?

One of the simplest budgeting methods is the EAB that works on the 50: 20: 30 rule.

• 50% of income for needs

• 20% for wants

• 30% for savings and investments

Is 50/30/20 a good budget strategy?

Yes, it is but the EAB is better and more geared for Expats in the UAE.

What is the golden rule of money?

The golden rule of money is pay yourself first! This means setting aside some of your money for savings before spending it on anything else

How do I budget as a couple or family?

Start by discussing your combined income, shared expenses, and financial goals. Create a joint budget that covers essential household costs, savings, and individual spending allowances. Regularly review the budget together to stay aligned and ensure both partners are comfortable with spending and saving decisions.

What should I do if I overspend my budget?

Don’t worry,overspending occasionally is normal and part of the learning process. Review where the extra spending happened, make small adjustments, and focus on staying consistent with your budget going forward. The goal is progress, not perfection, and each review helps you improve your financial discipline over time.