Debt Payoff Calculator UAE — Plan Your Path to Financial Freedom in AED

If you’re juggling a credit card, personal loan, car finance, or mortgage in the UAE, paying them off in the wrong order can cost you tens of thousands of dirhams in unnecessary interest.

This free debt payoff calculator, built for UAE residents and denominated in AED, shows you exactly when you can be debt-free, how much you’ll save with the right strategy, and how an extra AED 500 a month can shave years off your timeline.

Enter your debts below to get started ↓

Know Exactly What You Owe — Then Pay It Off Smartly

Every rocket launch starts with calculations. List your debts below, then choose a strategy to see how fast you can become debt-free.

1. List Your Debts

| Debt Name | Type | Balance (AED) | Rate % | Months Left | Min / EMI (AED) | Due Date |

|---|

2. Choose Your Strategy

Avalanche

Pay highest interest rate first. Saves the most money.

Snowball

Pay smallest balance first. Builds momentum.

Custom

Pay in the order you’ve listed the debts above.

3. Your Payoff Order

4. Repayment Schedule

Get Your Personalised Debt Plan

Enter your details to download a PDF copy of your full payoff plan.

How This Debt Payoff Calculator Works

The calculator runs a month-by-month simulation of your debts using your real numbers — balance, interest rate, months remaining, and minimum payment or EMI. Every figure is in AED, structured to match how UAE banks (Emirates NBD, ADCB, FAB, Mashreq, HSBC, Abu Dhabi Islamic Bank, and others) issue credit. When one debt clears, its full monthly payment automatically cascades into the next debt in your chosen order — the "cascade effect" that dramatically accelerates payoff.

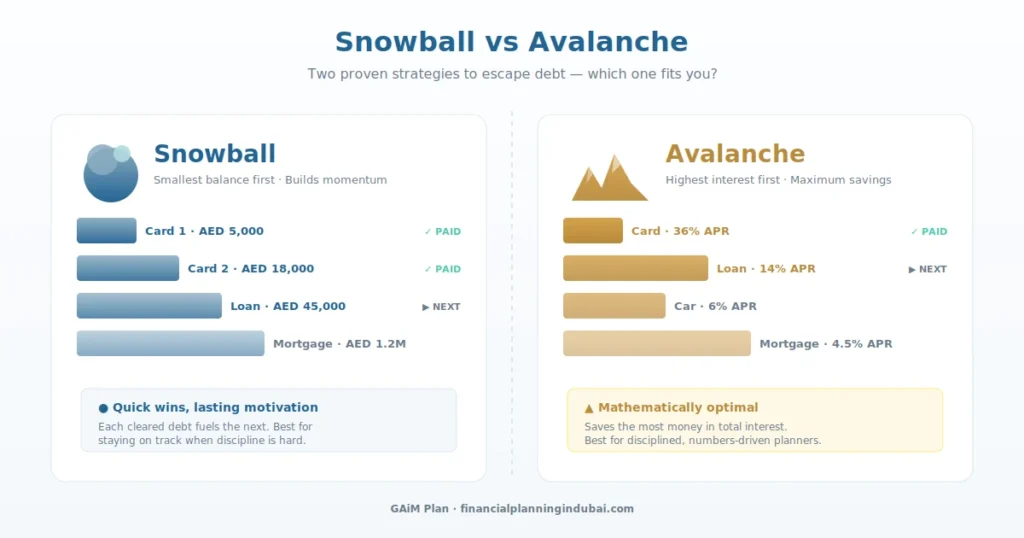

The Three Debt Payoff Strategies Explained

Avalanche Method

Direct any extra money to the debt with the highest interest rate first while paying minimums on the rest. This is mathematically optimal: it saves the most money in total interest. Best for disciplined planners who are motivated by efficiency and final numbers.

Snowball Method

Pay off the smallest balance first regardless of interest rate. Each cleared debt delivers a psychological win and builds momentum. Best if you've struggled to stay on track with previous attempts — the visible progress matters more than the maths.

Custom Order

Pay debts in the order you've listed them. Useful when you have specific reasons to prioritise certain debts: a co-signed loan, a debt to family, an account affecting your credit score, or one tied to employment.

Why Debt Strategy Matters in the UAE

UAE credit costs vary dramatically across product types:

- Credit cards typically charge 30–43% APR — among the highest in the world

- Personal loans average 6–14% APR

- Car loans sit around 4–6% APR

- Mortgages range from 3.99–5.5% APR

This spread means the order you tackle debts in can swing your total interest cost by AED 50,000 or more over a few years. For UAE expats earning tax-free income, every dirham going to interest is a dirham not building wealth.

Should You Include Your Mortgage?

Yes — and this calculator does. Many UAE expats keep mortgages separate in their thinking, but including it gives you the full picture. Even modest extra payments toward a mortgage early in its term can save hundreds of thousands of dirhams in interest. The calculator shows you exactly how much.

Common Questions

Will paying minimums clear my credit card?

Often, no. UAE credit card minimums (typically 5% of balance) can take 15+ years to clear a card carrying 36% interest. The calculator flags any debt where the minimum barely covers monthly interest.

Is debt consolidation always better?

Not always. A consolidation loan helps only if the new rate is meaningfully lower than your weighted average — which the calculator displays. Run your numbers first.

What about end-of-service gratuity or bonuses?

Lump sums applied to high-rate debt are usually the highest-return "investment" available to UAE residents. Use the extra payment slider to see the impact.

Next Steps

Once you've run your numbers, download your personalised PDF plan and review it monthly. If you'd like to see how clearing debt fits into your broader financial plan — protection, investments, and retirement — book a complimentary discovery call.