How to Invest in Index Funds in UAE: A Step-by-Step Guide (2026)

If you have ever felt that investing is only for people with a Bloomberg terminal and a finance degree, this “how to invest in index funds in UAE guide” is for you.

Index funds are the most cost-efficient and time-efficient wealth-building tool the investment world has produced. You buy one fund, you instantly own hundreds of companies, and you pay a fraction of what an actively managed fund costs.

For UAE expats, who already enjoy zero income tax and zero capital gains tax — index funds turn into one of the most powerful compounding machines available anywhere on the planet.

This guide walks you through exactly how to do it: which funds to look at, which platforms to use, the tax traps to avoid, and how to build a portfolio that survives the next market crash without you needing to lose sleep over it.

💡 Quick Answer

UAE residents can invest in index funds through a regulated brokerage (Interactive Brokers, Saxo Bank), an offshore platform (Ardan, Zurich International), or a regular savings plan.

The most tax-efficient route for expats is UCITS-domiciled ETFs listed on the London or Irish stock exchange — these avoid the 30% US dividend withholding tax and US estate tax exposure.

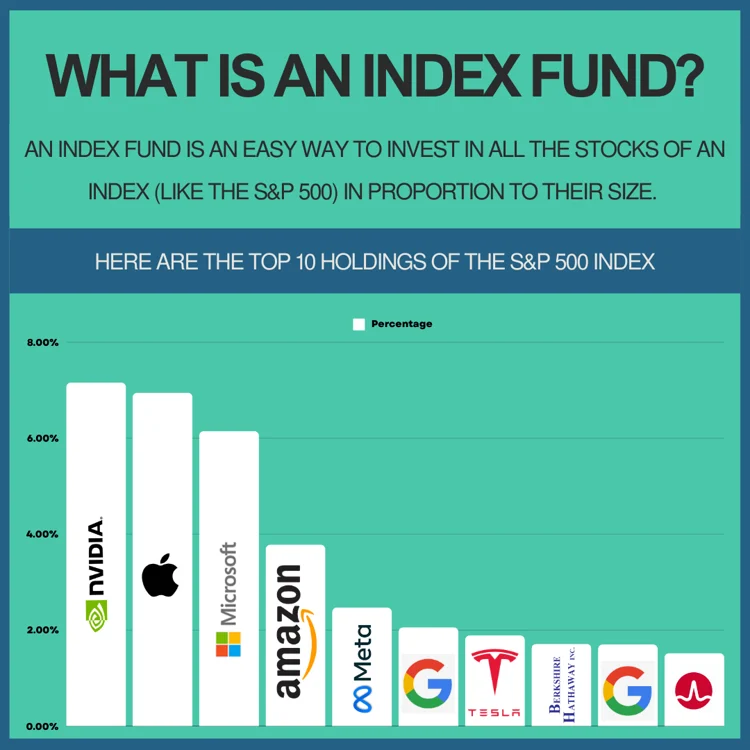

What Is an Index Fund?

An index fund is a basket of investments that mirrors a stock market index. For example, the S&P 500 (the 500 largest US companies) or the MSCI World (around 1,500 companies across 23 developed countries).

Instead of picking individual stocks, you buy one fund and you own a slice of every company in that index. If the index goes up 10%, your fund goes up roughly 10%. If it falls, your fund falls with it.

Why this matters in the UAE: Most expats here are time-poor, well-paid, and want their money to grow without becoming a second job. Index funds are built for exactly that profile.

Index Fund vs ETF — Are They the Same?

Almost. An index mutual fund is bought once a day at the closing NAV. An index ETF trades on an exchange like a stock, you can buy or sell any time the market is open. For UAE residents, Index funds are usually the better choice because they are more tax efficient, especially if they are help in platforms like Ardan.

Why Index Funds Work So Well for UAE Residents

Three reasons make the UAE a near-perfect environment for index investing:

- No income tax, no capital gains tax, no dividend tax. Whatever your fund earns, you keep — assuming you stay tax-resident in the UAE.

- Strong dirham (pegged to the USD). You can invest in dollar-denominated funds without worrying about currency erosion.

- Access to global markets. UAE-based investors can open accounts with brokers that give them access to the US, UK, European, Indian, and emerging market indices — often from a single dashboard.

The 7 Types of Index Funds UAE Investors Should Know

| Type | Tracks | Best For |

|---|---|---|

| Equity Index Funds | S&P 500, MSCI World, FTSE 100 | Long-term growth, retirement |

| Bond Index Funds | Global aggregate bond indices | Capital preservation, retirees |

| Sector Index Funds | Tech, healthcare, energy | Thematic conviction plays |

| Dividend Index Funds | S&P Dividend Aristocrats | Passive income seekers |

| Regional Index Funds | India, China, GCC, MENA, EM | Geographic diversification |

| Style Index Funds | Growth, value, small-cap | Tactical tilts |

| Commodity Index Funds | Gold, oil, broad commodities | Inflation hedging |

Index Funds vs Active Funds: The Honest Comparison

| Particulars | Index Funds | Active Funds |

|---|---|---|

| Goal | Match the index | Beat the index and generate better risk adjusted returns |

| Annual fee (TER) | 0.03% – 0.30% | 1.0% – 2.5% |

| Long-term winners (15+ years) | ~85–90% beat their active peers | ~10–15% beat their index |

| Manager risk | None | High |

| Tax efficiency | High | High |

| Effort to monitor | Moderate to Significant | Moderate |

“Active funds are not always wrong. They have a place in niche, inefficient markets; small-cap emerging markets, frontier markets, certain credit strategies. But for core US, global, and developed-market exposure, the data is overwhelming: index funds win.

Tax Considerations Every UAE Expat Must Understand

This is the section most blogs gloss over. Get this wrong and you can lose 30% of your dividends or expose your family to a six-figure US estate tax bill.

✅ The Good News

- No UAE income tax on investment returns

- No UAE capital gains tax

- No UAE dividend tax

- No UAE inheritance or estate tax

⚠️ The Trap: US-Domiciled ETFs

If you buy a popular US-listed ETF like VOO, SPY, or VTI, you are subject to:

- 30% withholding tax on dividends (no US-UAE tax treaty to reduce this)

- US estate tax on holdings above USD 60,000 if you pass away — at rates up to 40%

✅ The Fix: UCITS ETFs

Buy the Irish or Luxembourg-domiciled UCITS version of the same ETF.

UCITS funds have a 15% dividend withholding tax internally (on US holdings), zero estate tax exposure, and are accessible through Interactive Brokers, Saxo Bank, and most offshore platforms.

NRIs Investing in Indian Index Funds

If you are an NRI in the UAE buying Indian index funds, watch for:

- Long-term capital gains tax in India (12.5% above ₹1.25 lakh as of 2024–25 rules)

- Rupee depreciation against the dirham (historically 3–4% per year)

- TDS at source on redemption

Workaround: Consider USD-denominated India ETFs or Actively managed Mutual Funds held through platforms like Ardan, or India-focused UCITS ETFs, which sidestep most of these issues.

Step-by-Step: How to Invest in Index Funds in UAE

Step 1: Build a Financial Plan First (Non-Negotiable)

Most expats skip this and regret it within five years. Before you buy a single unit, you need clarity on:

- Emergency fund — 3 to 6 months of expenses parked in a high-yield UAE savings account

- Goals — what is the money for? Retirement at 55? A villa in Goa? Kids’ education in 2034?

- Time horizon — anything under 5 years should not be in equities

- Risk tolerance — can you stomach a 30% paper loss without panic-selling?

This is exactly what the GAiM Plan framework is built to solve — a structured financial planning process that maps your cashflow, balance sheet, goals, insurance gaps, and investment buckets onto a single plan before a single dirham gets invested. It is the difference between investing with intent and investing on hope.

Step 2: Define Your Investment Objective

Pick the dominant objective for each pot of money:

- Growth → Equity-heavy index portfolio (e.g., 80% global equities, 20% bonds)

- Income → Dividend-focused ETFs and bond index funds

- Wealth Preservation → Low-volatility and short-duration bond indices

You can run multiple objectives in parallel — just keep them in clearly separate accounts or “buckets” so you do not accidentally raid your retirement pot to fund a holiday.

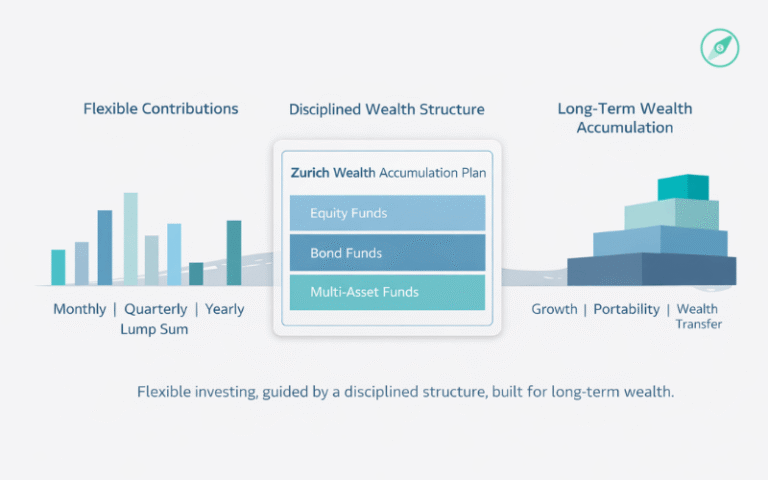

Step 3: Open the Right Investment Account

| Investor Type | Recommended Platforms |

|---|---|

| DIY investor, low cost focus | Interactive Brokers (IBKR), Saxo Bank |

| Wants advisor support + global access | Ardan Wealth Platform |

| Long-term saver who wants automation | Regular Savings Plans via Zurich International, MetLife, or Sukoon |

Step 4: Build a Robust Portfolio

A simple but powerful starting framework for a UAE-based expat with a 15+ year horizon:

A simple but powerful starting framework for a UAE-based expat with a 15+ year horizon is a diversified, multi-asset portfolio — not a single fund, not a single market, not a single currency.

A typical structure blends:

- A core global equity allocation for long-term growth across developed markets

- A regional or thematic tilt (US, India, emerging markets, technology) based on your conviction and goals

- A bond and fixed-income sleeve to dampen volatility and protect capital as you approach milestones

- Optional alternatives — gold, REITs, or commodities — as inflation hedges

Choose your funding style:

- Lump sum — best if markets are at fair value and you have cash sitting idle

- SIP / monthly contribution — smooths volatility, builds discipline, ideal for salaried expats

- Hybrid — invest 50% as lump sum, drip-feed the rest over 6–12 months

Step 5: Review, Rebalance, Realign

Index investing is passive — but not zero-effort.

- Annual review — check fund TERs, tracking error, and goal progress

- Rebalance — once a year, sell some of what is up and buy what is down to return to target weights

- Realign — major life events (marriage, kids, property purchase, return migration) should trigger a portfolio review

Common Mistakes of Index Fund Investment in UAE

- Buying US-domiciled ETFs by default — costs you 15% extra on dividends and creates estate-tax risk

- Chasing last year’s winners — picking the best-performing index of the past 12 months almost always disappoints

- Stopping SIPs during market falls — exactly when you should be buying more

- Holding too much UAE/regional equity — concentration risk in a market that represents <1% of global market cap

- Buying a Insurance linked investment plan for your investment goals.

- No exit strategy if you leave the UAE — your tax status changes the moment you become resident elsewhere

FAQs

Can expats invest in index funds in the UAE? Yes.

UAE residents — citizens and expats alike — can invest in index funds through international brokers like Interactive Brokers and Saxo Bank, or through advisor-led platforms such as Ardan Wealth.

Are index funds taxed in the UAE?

There is no UAE tax on investment income, dividends, or capital gains for individuals. However, US-domiciled funds carry a 30% dividend withholding tax and US estate tax exposure, which is why UCITS-domiciled ETFs are usually preferred.

What is the minimum amount needed to start investing in index funds in Dubai?

You can start with as little as USD 500–1,000 through regular savings plans. if you prefere investing a lump sum, you can start with USD15,000.

Which is better — index funds or mutual funds in the UAE? It depends on the market.

For developed markets (US, Europe, global), low-cost index funds tend to outperform most actively managed mutual funds over 10+ years, largely because of the fee gap. But in less efficient markets — India, China, and many emerging markets — several actively managed mutual funds have consistently delivered superior returns over long periods. A balanced portfolio often blends both: index funds for core developed-market exposure, and selectively chosen active funds for emerging markets and niche strategies.

Is the S&P 500 a good investment for UAE residents?

The S&P 500 has delivered roughly 9–10% annualized returns over the long run.

How do I buy the S&P 500 from Dubai?

If you are a DIY investor you can open a brokerage account with Interactive Brokers, Sarwa or similar trading platforms. If you want to work with an advisor, please connect with me for Holistic Financial Planning and a robust investment strategy.

What is a UCITS ETF and why does it matter for UAE expats?

UCITS stands for Undertakings for Collective Investment in Transferable Securities — a European regulatory framework. UCITS ETFs domiciled in Ireland or Luxembourg are far more tax-efficient than US-domiciled ETFs for non-US investors, including UAE residents.

Ready to Start? Let’s Make It Simple.

Index investing is simple, but simple is not the same as easy. The right fund choice, the right platform, the right contribution rate, and the right tax structure will determine whether you retire ten years earlier — or ten years later — than you planned.

I have helped over 350 expats from 50+ countries build clean, low-cost, tax-efficient portfolios from the UAE. No commissions on index funds. No pressure. Just a structured financial plan and a portfolio you actually understand.

👉 Book your free 30-minute Discovery Call

We’ll review your current investments, identify any tax traps, and map out a plan tailored to your goals.

Damodhar Mata is a Senior Financial Advisor and Sales Manager at Nexus Insurance Brokers LLC, Dubai, and the founder of GAiM Plan. Cert CII (UK), 14+ years advising UAE expats.

Disclaimer: This article is for educational purposes only and does not constitute personalised financial, investment, or tax advice. Past performance is not a reliable indicator of future returns. Always consult a regulated financial advisor before making investment decisions.